Introduction to Sharky.fi

Sharky.fi’s lending platform allows NFT holders to take out or issue loans against a preapproved Solana NFT collection.

Sharkyfi considers itself a hybrid lending protocol with a live open order book.

Users can get Solana loans, and later they will add the ability to issue stable coin loans such as USDC.

The loans are escrow less, meaning they will be kept in the user’s wallet without giving it up.

Unless the borrower defaults on their loan. It gives the lender the right to take the asset as collateral.

This is especially good for collections earning passive income that depend on taking snapshots for payouts.

Or it will allow holders to remain in their DAO when the Matrica refresh happens in discord. You get the idea…

Shark.fi, in essence, solves one of the liquidy problems with the Solana NFT ecosystem by unlocking and extracting floor value through their service.

Before I get started, let me clarify that we did participate in the presales on their NFT round of raises.

I also actively issue loans, so I’m a lender on the platform.

With that said, my thesis on them does not waver or change.

Now, let’s get into the details…

The collection size is 10,111 and about half was sold during the presale event.

Here is the wallet where the presale funds went into.

About 7 days ago, they transferred most of the (-11,366) mint funds out.

https://solscan.io/account/25HDbB1m7Hi3KXqA8W3BinTfk7eBH2RvJoagciaCFpbN#solTransfers

It’s become standard practice for these more extensive collections to oversubscribe their allowlist.

It minted out on BitFrost, a launchpad product by BlockSmith labs, with some hiccups.

I still hold all my Sharx and plan to keep them for their dual rev share.

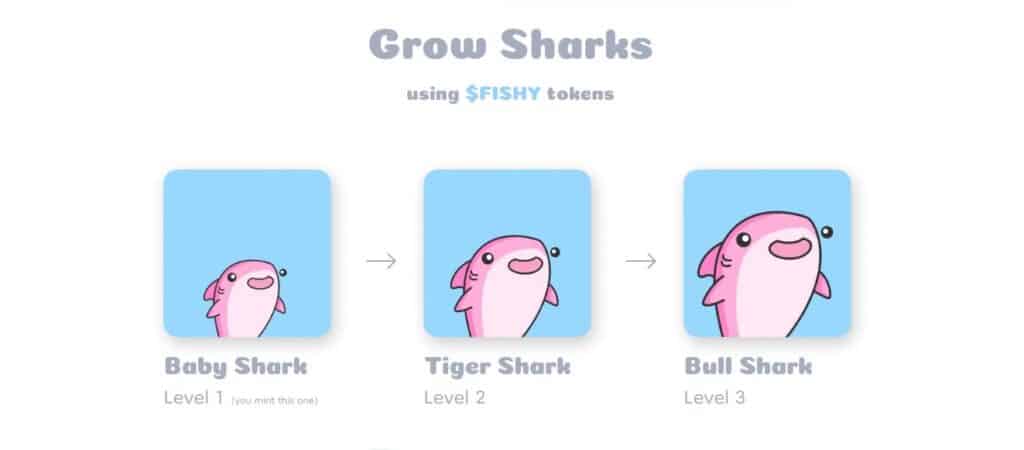

To become eligible, holders must use their native token, $fishy, to grow their Sharx to phase 3. It’s gamified.

Product to Market Fit and Revenue

There are no fees at this time to build users on the platform.

Based on a personal conversion during our vetting process with the founder, we estimate that the fees will be less than or equal to 1%. It’s unclear who will pay the loan origination fee.

Nonetheless, this platform will mainly gather revenue from fees generated through lending.

I have read that there may be another revenue stream by receiving a % interest fee earned on 3rd party liquidity.

During a Twitter space, one of the founders mentioned they have about 3 million dollars in loans and are aiming to be one of the top lenders in the Solana ecosystem.

Compostability/integration plays planned have already been seen in the wild on their BitFrost mint page, where users could borrow against their NFTs to fund their mint.

They had a promo where if you did use this integration to fund your mint, you would get .5 $SOL back. As long as the Sharx was not transferred from the minting wallet and the loan promise was fulfilled.

Each token swap cost during mint was about 0.00947 ◎ on the high side for Solana gas.

There are two use cases for Sharky. You could either be a lender or borrower on their platform.

Lend

When one lends, you make money on the interest tacked on at the time of issuance.

The loans use a simple model of a static interest rate.

The interest amount looks dynamic on a sliding scale, and the loan term is either 7, 14, or 16 days (depending on the collection).

I’m unsure how these numbers are figured out, and I’ll update you once I have more information.

How Do I Know How Much to Lend out On the Collection?

Before giving you info on how many points below the floor you should lend, let’s discuss the potential downsides and upsides.

The issue with lending in the new web3 is that there are no reliable credit checks in the Solana NFT space. Atadians is working on resolving this; however, it’s far from a working product.

Lending Tools

As a good entrepreneur, one may think, ok, now that I can earn .30 SOL for a lending contract. How can I do this 1000 times over?

The founder Restuta hinted that they will be releasing some internal lending tools they use to lend out their funds.

This is an area that lenders should pay attention to and even develop their own tools for lending and going a step further and providing it as a crypto SaaS.

How to Lend

Lending is super easy.

Go to the lending tab.

Select the NFT collection you’d like to lend to by clicking “Lend” next.

Pay close attention to lending duration, as you will commit to that loan duration.

Some collections have a lending duration of as long as 16 days. However, most are either 7 or 14 days.

You can have your lending strategy, but here’s a sample to give you an idea.

Lend out only to collections you would like to own if the borrower defaults.

Check the floor price on an aggregator such as hyperspace to get the lowest floor price.

Now you have your ceiling price for the loan.

Adjust price for % downside price action. As this will be your loan amount.

Now you have your new ceiling price. This will be the max you should lend out.

Check the order book on the collection to see what lenders are quoting and offer a competitive loan that’s competitive.

Don’t let FOMO set in if lenders are offering higher loans. Stick to your lending principles, and your loan will eventually get picked up.

It’s good to be familiar with the collection you’re lending out because you’ll know the price drivers.

Place your offer and wait for someone to borrow from you.

Borrow

Borrowing goes the same way.

Visit the borrowing tab, select the collection you want to borrow, and click borrow.

Select a suitable offer.

Pay back your loan plus interest and get your collateral NFT back.

Downside Protection

Should I call this section “How to Short your Solana NFT”?

If you think the price action for a particular NFT will be down.

Then you could take a loan out and let it default.

This is how you can short an NFT using their platform.

Second Round of Funding

During our due diligence, we found information on metaCOLLECTIVE that they were raising a token sale in late January.

The ticket size was $25-50k at a $40m valuation. Tokens come with 1y vesting + 18 months linear unlock.

Was this their first round of funding? Probably not, as the document mentions some VCs (angel investors) and totes partnerships with Mango Markets and Holaplex.

Recent NFT Raise

As mentioned earlier, their 10,111 collection and mint price of 2.9 for the public.

We can estimate their raise was about 29,321 $SOL.

The price of SOL is ~$33, bringing the raise to about $967,622.

Their royalty for their NFT is set at a whopping 7.9%.

These are rough estimates as the collection had different tier pricing for their presale, allowlist, and public minting phases.

Native $fishy Protocol Token

Stakeless staking was announced today, and they will start accumulation today. Sharky.fi will begin its distribution in 30 days, possibly due to the 30 vesting period with the linear unlock we had to agree to during presale.

There isn’t much posted about their tokenomics at the moment. However, from my understanding, $FISHY will upgrade the NFTs to level 3 Sharx, where they start to earn dual rev share.

Dual revenue sharing is where they will share a % of their platform fees and royalties from secondary market sales go to a pool, and holders extract the value from the liquidity pool.

I suspect this is where their token will get its value from, and the token investors will be able to get their return.

Returns to Holders

So you’ve probably heard that they have revshare.

Their revshare will be a percentage of fees accrued on the platform, plus the royalties from the secondary market sales.

It sounds like they’ll put it into a pool, and holders will get their share.

To become qualified for this dual revshare, you must have held your Sharx long enough to earn enough $fishy to upgrade the little shark to level 3.

The exact numbers are unknown, but here is some information to give you ideas on what the operator expects to pay out.

Our back-of-the-napkin calculations correlated with these numbers, so I feel confident posting them.

They aren’t yet ready to publish exact tokenomics, but they are going to share revenue from platform fees (25%) and royalties (% tbd, 25-50)

30 NFTs should produce enough $FISHY tokens to upgrade faster than most and get more rev share, but the exact math of that is complicated; here are the broad strokes:

Math is a bit complicated (intentionally) because it depends on how exactly you use your Sharx and upgrade them.

My estimate says that given our current revenue and projected 2nd trading volume (conservatively), we should be able to generate enough revenue to pay off all NFTs in ~29 months (yes, all 10k sold), but likely much faster because they are growing.

They will have non-linear revenue distribution, basically where the biggest supporters would get more revenue, since they took a more considerable risk, invested more time and/or funds, short term and investment.

According to my math, the initial mint should be paid off in 4-5 months.

We’re not even accounting for the price of NFTs on the market at the time) depending on allocation and strategy.

This is the intent, so the best investors, players, and platform users will get returns faster.

Then over time, smaller holders will start making more and more revenue making distribution close to uniform at a later stage.

It’s an experimental model that they believe is more sustainable.

However, it might look like it is more beneficial for whales, I think it’s a tricky balance, and mid-long term, it’s better for retail as well, since without strong diamond hands and their support project will be less successful.

Their model tries to help with even more capital distribution as time passes.

Note: We estimate .5-1 sol per week payout for the minimum ticket size of 30 Sharx.

Final Thoughts

The concept Sharky delivers on isn’t new in the ecosystem. There are few pawnshop-style projects, but their execution has been excellent.

What the future holds for them and lending, in general, is uncertain due to the sheer speed of crypto expansion on a macro level.

The next phase in the Defi/NFT space is AMM (Automated Market Making), and the next player to be able to do it with loans will set a new tempo.

This is because, right now, it’s up to the borrower to select the offer. This can be automated through an automatic pool. However, the downside to this would be a centralized lending pool where the users may not get the best deals.

Meaning the loan-to-value will naturally be much lower in these pools.

In the previous example, Elixr comes to mind.

A lite implementation of AMM could work as such…borrower defaults, lender gets the collateral, then it autosells using AMM stream lining the entire process while not leaving the ecosystem.

Once Sharkyfi lends out Solana and USDC, they may chase a cross-chain ambition.

We hope to see Sharky adapt itself and remain in the running lead.

The lending platform is impressive with its 3,650 active wallets, and an estimated 8899 $SOL paid directly to lenders.

Their loan default rate is just above 3%, still below the 4% industry average.

As their volume grows, we expect the default rate to rise.

All this has been accomplished with only 184 NFT collections verified and more added daily.

An NFT enthusiast and a crypto early adopter, Bodi is the editor in chief on RareBot.com. He is joined and assisted by a team of NFT fans and experts bringing you the latest news in the industry. He is a finance major with 20 years of experience and education in tech and banking.